We have heard countless times over the past few years how badly Bernanke has debased the US Dollar. In certain terms he has done this. The claim that the USD would be higher in the absence of QE is counter factual at best. Who knows where the USD would be if the Fed never expanded its balance sheet. One can claim that the USD would be higher on a trade weighted basis because of the Euro's woes. This would equal out the Yen's rise in the same period. My guess is that the USD would have remained weak. The USD was a weak currency before QE and the credit crisis and its certainly a weak one now. This is so because the USD has massive structural problems and headwinds. We have an uneven trade policy on top of a non existent fiscal policy that renders the Dollar to be go no where but down. We run huge trade deficits that need to be financed through deficit spending. Now deficit spending is an accounting term yet it is still a figure. We simply don't have enough revenue coming in to make up for entitlement spending, defense spending, bailouts, and lack of taxes.

The Fed has tried to make up for the lost output by starting up speculation via Animal Spirits. The Fed's QE and ZIRP programs have only succeeded in creating more confusion in the way monetary policy actually functions. Monetary policy in the midst of a balance sheet recession is completely impotent and useless. The Japanese know this. It doesn't matter how low rates are if the banks/private sector can't find profitable investments to sink them in to. The ZIRP the Fed has instituted is basically a sinking fund for Wall Street speculation. We have seen commodity prices sky rocket. We have seen equity prices also rise. In fact all risk assets are rising in the same direction. This is a dangerous correlation. What goes up during QE has to come down when the policy ends. This is what we have seen.

What the Fed is doing is technically not money printing as much of it is an asset swap. The Fed can't print money. It has no authorization to do such a thing. Its the Treasury that does the printing if any printing is actually done. The Fed sits under the Treasury and what the Fed does is simply credit bank accounts electronically. This is how they manage the monetary base and the reserves in the banking system. Through Open Market Operations they add or subtract via Repo's / Reverse Repo's, monied reserves. Through the interest rate channel they set the discount rate and put a target on the Fed Fund's Rate. This is all they do. My problem is a ZIRP policy is destroying savings at a time when the country needs to have some sort of return for their fixed rate investments. Its stoking speculation into risk assets when the private sector most notably consumers need to deleverage and pay off debts. Super low rates gave us a credit crisis as many used their homes as ATM's. We need to move to a more normalized interest rate policy.

What the Fed tried to accomplish through QE was just an asset swap of taking out interest bearing assets from the capital markets and parking them inside the Fed. The Fed basically is taking out higher interest bearing coupons and making investors invest in lower coupon. As the Fed pushes the curve down while keeping rates at zero, effectively controlling the entire curve. If this is not central planning I don't know what is. The entire market is captured by short term zero bound rates while long term rates are pushed down by a weak economy and other deflationary forces. Its this dynamic I have stated previously that is killing savers while enriching speculators. Its this Reverse Robin Hood policy instituted by Bernanke that has become the 1 Million pound elephant in the room. This is the monster that he has created and the monster gets bigger and more difficult to manage as time goes by. Now the Fed not only owns Treasuries but a Trillion dollars worth of high coupon MBS. What they wanted to do was take the high coupon MBS out of the market, push rates down so that refinance activity picks up. Which is a noble idea except rates are going down but so is general housing prices. Rates are down not because the Fed is buying but by a general lack of interest and demand for housing. No one can get approved and many are stuck in under water homes that can't be refinanced. Oh! did I mention 9% unemployment? Even if refinance activity picks up and higher coupon MBS that the Fed owns are paid down, this by itself is deflationary. Deflation is the bogeyman for the Fed. They instituted QE2 because of it. They are sowing the seeds for more deflation with their policies.

Along with the fact that Bernanke had zero clue about where the economy was going in 2008 and his subsequent Housing is contained speech on CNBC. They all say that you can't fight the Fed but you can pretty much bet against Ben at every turn.

http://tradersutra.blogspot.com/2010/12/bet-against-bernanke-surely.html

Of late Ron Paul and now Texas Gov. Rick Perry are on Bernanke's case about the Dollar. This is the same Rick Perry who takes credit for the Sun coming up in Texas every morning. He has no clue about monetary policy or the drivers of the general economy, all of which probably makes him a better candidate for President. Both Paul and Perry have been hammering Bernanke over the Dollar. They should be hammering him about ZIRP. What ever Bernanke is doing to the Dollar is nothing compared to what Congress has already done. Again, the Fed doesn't set Trade or Fiscal Policy. That is done by Congress and the White House Administration. Both of these branches of government has sold out the country to big business which wants a lower dollar to export out.

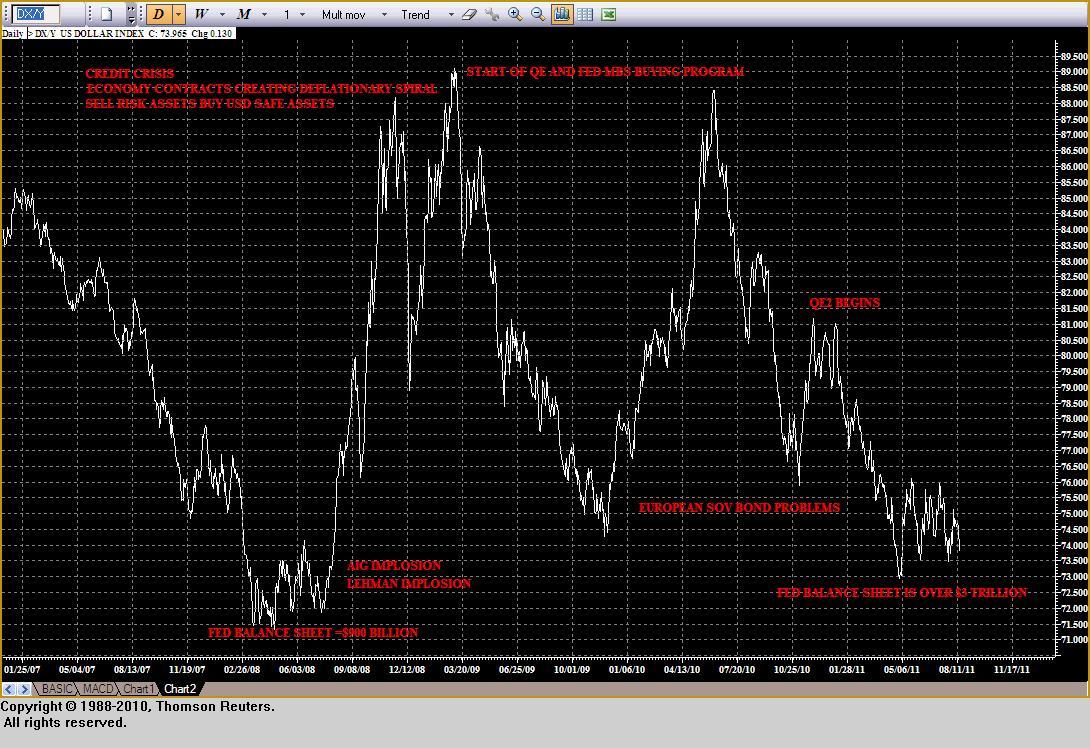

The Fed's QE and expansionary balance sheet maneuvers are asset swaps only. The Fed's balance sheet has gone from less than $900B to over $3T since 2008. Many have mistakenly stated that he has greatly expanded the money supply. Which after closer examination really is not the case.

The following charts from from ShadowStats.com;

http://www.shadowstats.com/charts/monetary-base-money-supply

The more important charts are these longer term money supply charts.

Courtesy Of Shadow Stats.

Bernanke has expanded the money supply, but not as much as people have previously (Myself included) have thought. Long term money supply growth is around 5%. Bernanke has expanded that over the last few years to 5.5%. Not a big deal compared with the Chinese who have expanded their funny money by 17% a year for the last 10 Years. They also peg their funny money to the USD to keep it undervalued, which they have to as they are an export led economy. They recycle the dollars from their trade surplus back into our economy via the Treasury Market. This is the global savings glut argument that many are making for the credit crisis. It has some logic to it but most of it is bogus rhetoric. The Chinese bought Treasuries hand over fist pushing long term rates down which enabled the housing credit crisis. This is the meme that many supply siders, deregulators, bank lobbyists, and Wall Street apologists are making. Sprinkle in some its all the poor's fault, the CRE did it, deadbeat homeowners, government housing policy, Yada Yada Yada, you get the picture. Zero accountability for elitist bankers, supply siders, deregulators, and bank lobbyists.

If it was all that simple and easy.

The primary reason we had a credit crisis was a total abdication of lending standards and total misplaced incentives by the banking sector. It was a hot potato credit fiasco created by Wall Street institutions. I still don't understand how in the world the CRE made AIG make all those bad CDS bets? How did the CRE make Lehman make all those bad RMBS and CMBS loans? Can someone please explain this to me?

Back to the USD. As you can see, The USD was lower in 2008 when the Fed's balance sheet was 1/3 the size. You can't blame the Fed entirely for the Dollars decline, you have to blame other government policy makers for that. You have to blame Congress for fiscal and trade policies and the White House for a total lack of attention to global economic affairs.

No comments:

Post a Comment